Buying a home in Noida is one of the biggest financial decisions you'll make — and one of the first questions every buyer faces is simple but important: should you pay cash, or take a home loan? Both routes can get you the keys to your new home, but they affect your finances very differently. Here's a clear breakdown to help you decide what works best for your situation.

The Case for Paying Cash

If you have the funds available, buying a property outright in cash has real advantages, especially in a market like Noida where many transactions — particularly resale and land deals — still happen this way.

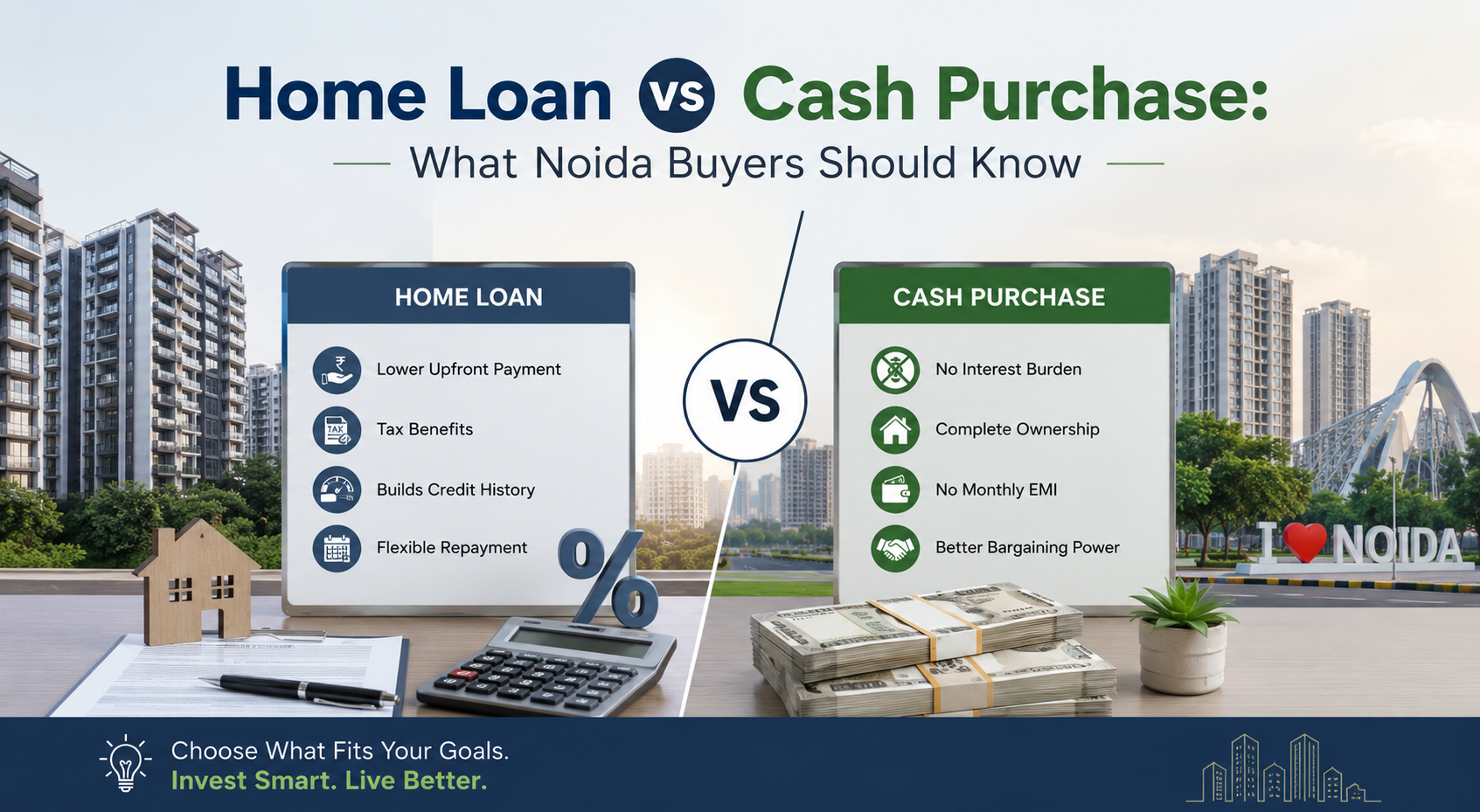

1. No Interest Burden The most obvious benefit is that you avoid paying interest altogether. Over a 15–20 year loan tenure, the interest component can sometimes equal or exceed the principal amount. Paying cash means the price you pay is the price you pay — nothing more.

2. Stronger Negotiating Position Sellers, especially in resale and under-construction deals, often prefer cash buyers because the transaction closes faster with fewer contingencies. This can translate into better price negotiation, particularly in sectors like Noida Expressway or Greater Noida West where inventory movement is competitive.

3. Simpler, Faster Transactions Without loan approvals, valuation reports, or bank disbursement timelines, a cash deal can close in weeks rather than months. This matters a lot if you're trying to lock in a property before a price revision or a builder's offer deadline.

4. No EMI Stress Without a monthly EMI, your cash flow stays flexible. This is particularly attractive for buyers nearing retirement or those who prioritize being debt-free.

The Trade-Offs of Paying Cash

The biggest downside is opportunity cost. Real estate in Noida, especially well-located projects, typically appreciates over years rather than overnight. If your cash could otherwise be invested in equity, mutual funds, or business expansion at potentially higher returns, locking it all into one property may not be the most efficient use of capital. You also lose the tax benefits associated with home loans (more on that below), and you concentrate a large portion of your wealth into a single, illiquid asset.

The Case for a Home Loan

For most salaried and self-employed buyers, a home loan isn't just a fallback — it's a deliberate financial strategy.

1. Preserves Liquidity Instead of locking ₹50–80 lakh (or more) into one purchase, a loan lets you make a smaller down payment — typically 10–20% — and keep the rest of your capital available for investments, business needs, or emergencies.

2. Tax Benefits This is where home loans become genuinely attractive for Indian buyers:

- Under Section 24(b), you can claim a deduction on home loan interest paid for a self-occupied property.

- Under Section 80C, principal repayment qualifies for deduction within the overall 80C limit.

- For first-time buyers, additional benefits may apply under sections like 80EEA, depending on the property value and loan amount — it's worth checking current eligibility with your CA, as these provisions are revised periodically in the Union Budget.

Together, these can meaningfully reduce your effective cost of borrowing, sometimes making the "real" interest rate significantly lower than the stated rate.

3. Builds Credit History A well-serviced home loan strengthens your credit profile, which can help with future borrowing — whether for a second property, business loan, or other financing needs.

4. Leverage for Long-Term Wealth Building Real estate in high-growth corridors like the Noida-Greater Noida Expressway, Sector 150, or areas benefiting from the upcoming Jewar Airport, has historically appreciated well. By using leverage (the bank's money) rather than all your own capital, your potential return on your invested capital can be higher, even after accounting for interest costs.

The Trade-Offs of a Home Loan

The obvious cost is interest — over the loan tenure, you will pay more than the property's purchase price. There's also EMI commitment, which adds a fixed monthly liability to your budget for years, and processing requirements like income proof, credit checks, and property valuation, which add time and paperwork to the purchase.

So, Which Should You Choose?

There's no universal right answer — it depends on your financial profile and goals.

Consider paying cash if:

- You have surplus funds without disturbing your other investments or emergency reserves

- You want to avoid all debt obligations

- You're buying for immediate end-use, not investment leverage

- You're getting a meaningfully better deal by paying upfront

Consider a home loan if:

- You want to preserve liquidity for other investments or business needs

- You can benefit from tax deductions under your current income bracket

- You want to build a credit history

- You believe your capital can earn better returns elsewhere than the loan's effective interest cost

A hybrid approach is also common and often sensible: making a larger down payment (40–50%) to reduce the loan amount and interest burden, while still preserving some liquidity and tax benefits.

A Few Practical Tips for Noida Buyers

- Always verify RERA registration of the project before finalizing payment, regardless of how you're financing the purchase. This protects you against delays and ensures the builder is compliant with disclosure norms.

- Compare loan offers across banks and NBFCs — interest rates, processing fees, and prepayment terms vary, and even a small difference in rate can add up significantly over a long tenure.

- Factor in additional costs — stamp duty, registration charges, GST (for under-construction property), and maintenance deposits apply regardless of how you pay, so budget for these separately from the property price.

- Get a property valuation done independently if possible, especially for resale properties, to ensure you're paying a fair market price.

Final Thoughts

Whether you choose to pay cash or take a home loan, the right decision comes down to your liquidity needs, tax situation, and long-term financial goals — not just which option seems "cheaper" on the surface. At GTB Realty, we help buyers across Noida, Greater Noida, and Faridabad evaluate both paths with clear, honest guidance tailored to their financial situation, so you can make a confident, well-informed decision on one of life's biggest investments.

Looking to buy in Noida or Greater Noida? Get in touch with GTB Realty for personalized guidance on financing options, RERA-verified projects, and the best opportunities across Delhi NCR.